Forward-Deployed Engineering Is the New SaaS

President, Zaruko

Table of Contents

Yesterday's post argued that AI breaks the SaaS replication engine and that the services model is the architectural escape hatch.5 The data that used to flow from clients to vendors and compound into a moat now sits behind contractual restrictions, so software replication economics are shifting toward services delivery for AI work. Forward-deployed engineering is what the labs are actually building. They placed two large bets on it in the past three months.

In February, OpenAI announced Frontier Alliances. Multiyear partnerships with Boston Consulting Group, McKinsey, Accenture, and Capgemini, built around its new Frontier platform, which OpenAI describes as an intelligence layer that stitches together enterprise systems and helps companies build and deploy AI agents.1 The financial terms were not disclosed, but the four firms are each building dedicated practice groups certified on OpenAI technology. OpenAI's forward-deployed engineers will sit alongside the consultants on client engagements.

On Monday, Anthropic announced something that looks similar on the surface and is structurally the opposite. A new AI-native enterprise services company formed jointly with Blackstone, Hellman & Friedman, and Goldman Sachs. Backed further by General Atlantic, Apollo Global Management, GIC, Sequoia Capital, and Leonard Green.2 Wall Street Journal reporting cited by Fortune put the committed capital at approximately $1.5 billion.2 Anthropic's applied AI engineers will be embedded directly. The target market is mid-sized companies. From the Anthropic press release: community banks, mid-sized manufacturers, regional health systems.3

The two announcements landed roughly ten weeks apart and reflect opposite theories of how to deliver AI inside the enterprise.

The press coverage has framed this as the AI labs entering the consulting business. That misreads what is happening. Neither lab cares about partner-hour revenue or PowerPoint margins. They are not trying to compete with McKinsey for advisory work.

They are extending into the application layer through a route that direct products cannot reach.

The Two-Front Application Strategy

Both labs have been building application products directly for the last 18 months. Anthropic has Claude for Excel, Claude for PowerPoint, Claude for Slack, Claude Cowork, and a financial services agent suite.4 OpenAI has ChatGPT Enterprise, Codex, and Frontier as its enterprise agent platform. These products attack horizontal workflows. The kind of work that looks similar across companies. Drafting a slide. Cleaning a spreadsheet. Triaging a ticket. Writing code.

Horizontal workflows behave well under the SaaS model. The product is broadly applicable. Customers do not need deep customization. Each new customer reinforces the same product roadmap, the same deployment patterns, the same reusable architecture and workflow templates. The replication engine still works, mostly.

The other half of enterprise software does not look like that.

A community bank's loan origination workflow is not a horizontal product. A regional health system's prior authorization process is not a horizontal product. A mid-sized manufacturer's quality assurance pipeline is not a horizontal product. These are deep, specific, embedded workflows that vary across institutions. The data is restricted. The integration requirements are bespoke. The work is the product, and the product is different at every site.

You cannot ship Cowork into a community bank's loan workflow. There may be a Claude-powered loan origination template, but the deployable system still has to be rebuilt around each bank's policies, data, controls, and core systems.

This is the application surface that direct products cannot reach. And it is by far the larger half. Sequoia partner Julien Bek's intelligence-vs-judgment framework, which I covered yesterday,5 lays this out: the largest service categories sit in deep vertical workflow. Insurance brokerage at $140-200B. IT managed services at $100B+. Healthcare revenue cycle at $50-80B. Claims adjusting at $50-80B.6 None of these get reached by shipping a horizontal SaaS product.

What reaches them is forward-deployed engineering. People who build a custom system inside the customer's environment. Each engagement is the application. The output is not a deck. It is a working AI system embedded in the bank's loan workflow, the health system's prior auth pipeline, the manufacturer's QA process.

This is exactly the AI-native services model from yesterday's post. The vendor is the operator. The data stays in the engagement. The replication engine works at services scale rather than SaaS scale. Six times the TAM, lower margins, structurally more defensible against the data restriction problem because the operator-as-vendor structure leaves procurement with far less to restrict.

OpenAI and Anthropic have decided this is where the second front of the application layer war is fought. They are placing different bets on how to staff it.

Same Destination, Opposite Strategies

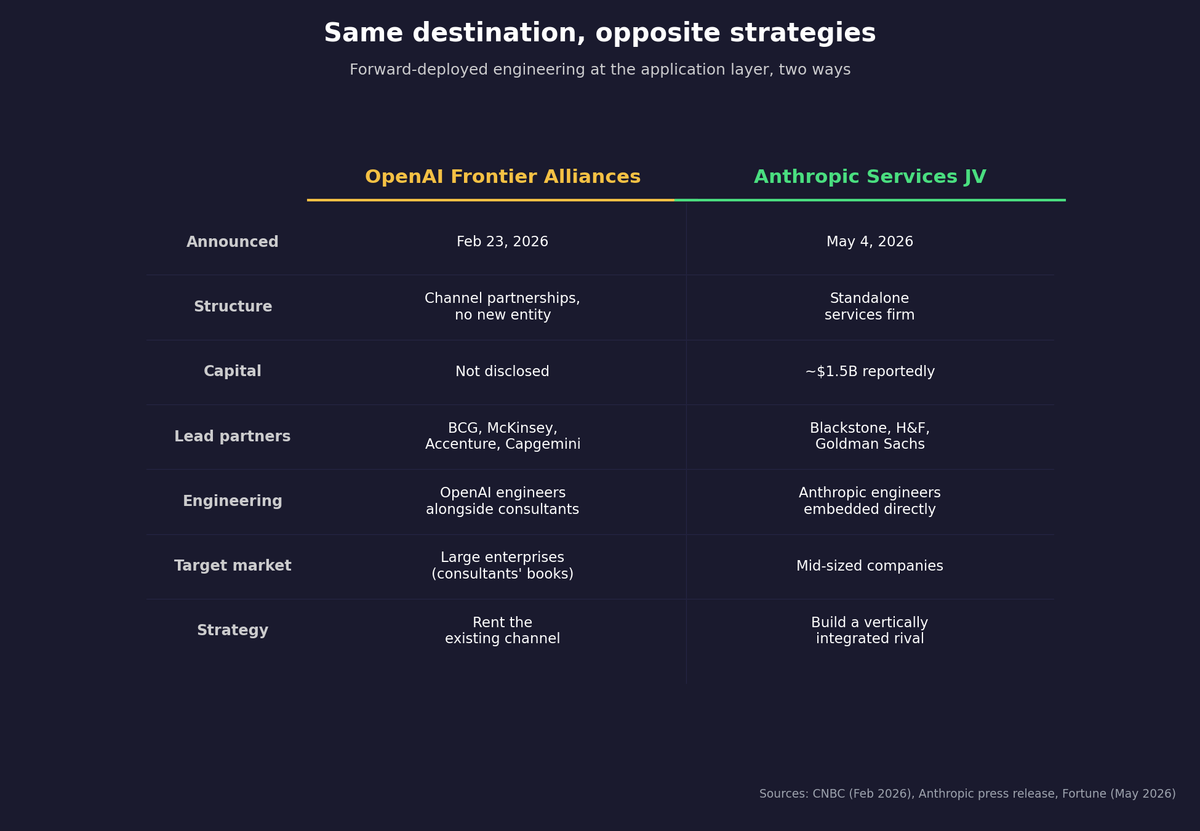

Figure 1: Structural comparison of OpenAI Frontier Alliances and the Anthropic services joint venture across seven dimensions. Both target forward-deployed engineering at the application layer; one rents the consulting channel, the other builds a vertically integrated rival. Sources: CNBC (Feb 2026), Anthropic press release, Fortune (May 2026).

OpenAI rents the consulting channel. The Frontier Alliances structure does not create a new entity. Four named consulting firms (BCG, McKinsey, Accenture, and Capgemini) are instead building certified practice groups around Frontier. BCG and McKinsey lead strategy and operating model work. Accenture and Capgemini handle systems integration. OpenAI's forward-deployed engineers slot in alongside them on engagements. The consultants keep their independence and their other partnerships. McKinsey already has a multi-year Gemini deal with Google Cloud.1 Accenture announced a sweeping Anthropic partnership in December 2025.1 Frontier Alliances is one more channel relationship for firms that have many.

Anthropic builds a vertically integrated rival. The new entity is a standalone services firm with its own engineering bench, capitalized to compete directly with the consultants. Blackstone President Jon Gray described the goal as breaking what he called one of the most significant bottlenecks to enterprise AI adoption: the scarcity of engineers who can implement frontier AI systems at speed.3 The implication is that frontier-AI engineering talent is the binding constraint and that the new firm is engineered around that scarcity rather than relying on existing benches to scale into it.

OpenAI's bet is that the four consulting partners already have the relationships, the bench depth, and the change-management muscle. Speed to scale matters more than ownership of the channel. Enlist them, certify them, embed engineers alongside them, move.

Anthropic's bet is that the existing consultants are too slow, too expensive, and not engineering-led enough to deliver application work at the pace and price the market wants. Better to build a new entity, capitalized by PE, designed engineering-first, with a built-in client pipeline through the sponsors' portfolios.

Both bets can be right at the same time. They are aimed at different segments. OpenAI's channel partners primarily serve large enterprises. Anthropic's new entity is explicitly aimed at mid-sized companies that have historically been priced out of frontier consulting work. Goldman's Marc Nachmann put the goal as democratizing access to forward-deployed engineers for companies that cannot afford the talent or the consulting fees.3

The bets reflect different reads of where the bottleneck sits. OpenAI is betting that the existing consulting bench has the depth and just needs Frontier certification, training, and OpenAI engineers embedded alongside. Anthropic is betting that frontier-AI engineering depth is the actual scarce input and that the existing benches do not have enough of it, so they are building a new firm that is engineering-led from day one.

What Mid-Market Operators Should Take From This

The Anthropic joint venture is, in plain language, built for you. The press release names community banks, mid-sized manufacturers, and regional health systems. The capital structure suggests an ambition to make this cheaper and more scalable than traditional consulting engagements with firms like McKinsey, BCG, or Bain. The PE consortium provides a built-in client pipeline through its portfolio. The Anthropic engineering bench provides the technical depth. The thesis is that a mid-sized company that could never have hired McKinsey for an AI transformation can now hire something that delivers the engineering output at a fraction of the cost.

That is the pitch. Whether the execution lands is a different question.

Forward-deployed engineering at scale is hard. Palantir is the proof point and it took them roughly 20 years to build that muscle. PE-backed services rollups have a mixed track record. The unit economics are not yet proven outside a few categories. Spinning up a joint venture of this scale does not mean the operating model works on day one, or in year three.

The right response is not to assume this venture wins. It is to recognize that the buy-vs-build decision your team has been having for the last two years now has a third option. Buy software. Build internally. Or hire an AI-native services firm to operate the function.

That third option did not exist as a credible answer for mid-market companies until this week. It does now.

The implication for procurement and strategy is concrete. The line items where you are already buying outsourced services in intelligence-heavy categories, such as IT managed services, tax, audit, claims handling, routine legal work, are the ones where the AI-native services pitch will arrive first. The mid-market AI vendor that calls on you in 2026 may not be selling software at all. They may be offering to run the function and bill you on outcome rather than per seat.

Your incumbent relationships in these categories are now competing with a different kind of vendor. One that did not exist when you signed your last MSA.

The Bigger Picture

The two announcements, read together with the Sequoia thesis, describe a coherent strategic shift at the foundation model layer.

The labs cannot capture most deep enterprise application work by selling APIs alone. The data will not flow back. The customization will not compound. The replication engine is broken at the foundation model layer the same way it is broken at the application layer. Going down the stack into services is the path to capture the $6 of services spend that sits behind every $1 of software spend.

Yesterday I argued that AI breaks the SaaS replication engine and that services is the escape hatch. The labs are not just observing this. They are funding it directly. OpenAI is renting the existing channel to move fast. Anthropic is building a new one to compete on price and target a market the existing channel never served well.

The next 18 months will tell us which bet works at scale, and probably both will work in different segments. What is not in doubt is the direction. The application layer is being captured through services. The mid-market is the segment where the impact will land first.

Sources

- Capoot, Ashley. "OpenAI lands multiyear deals with consulting giants in enterprise push." CNBC, February 23, 2026. cnbc.com. ↑ ↑ ↑

- Lichtenberg, Nick. "Anthropic takes shot at consulting industry in joint venture with Wall Street giants." Fortune, May 4, 2026. fortune.com. ↑ ↑

- Anthropic. "Building a new enterprise AI services company with Blackstone, Hellman & Friedman, and Goldman Sachs." May 4, 2026. anthropic.com. ↑ ↑ ↑

- Anthropic. "Agents for financial services." 2026. anthropic.com. ↑

- Damianakis, Stefanos. "AI Broke SaaS. Services Is the Escape Hatch." Zaruko, May 7, 2026. zaruko.com. ↑ ↑

- Bek, Julien. "Services: The New Software." Sequoia Capital, March 2026. sequoiacap.com. ↑

Frequently Asked Questions

What is forward-deployed engineering, and why is it the new SaaS?

Forward-deployed engineering is the practice of placing engineers from a software vendor inside a customer's environment to build a working system around that customer's data, policies, and core systems. Palantir made this model famous over roughly 20 years. With AI, the same pattern is becoming the way the foundation model labs reach the deep enterprise application work that horizontal SaaS products cannot. The replication economics shift from software (build once, sell many) toward services (build once per engagement), but the resulting work is structurally more defensible against enterprise data restrictions because the operator-as-vendor structure leaves procurement with far less to restrict.

How is OpenAI's Frontier Alliances strategy different from Anthropic's services joint venture?

OpenAI is renting an existing channel. Frontier Alliances are partnerships with BCG, McKinsey, Accenture, and Capgemini, with OpenAI engineers embedded alongside the consultants on engagements. No new entity, no new capital structure, target market is large enterprises served by the four firms. Anthropic is building a vertically integrated rival. A standalone services company formed with Blackstone, Hellman & Friedman, and Goldman Sachs, reportedly capitalized with approximately $1.5 billion, with Anthropic's applied AI engineers embedded directly. Target market is mid-sized companies that have historically been priced out of frontier consulting work. Same destination, opposite strategies.

What does the Anthropic enterprise AI services joint venture mean for mid-market companies?

It introduces a third option to the buy-vs-build conversation that has dominated mid-market AI strategy. Buy software, build internally, or hire an AI-native services firm to operate the function. The joint venture with Blackstone, Hellman & Friedman, and Goldman Sachs is explicitly aimed at community banks, mid-sized manufacturers, and regional health systems. Companies that historically could not afford McKinsey or BCG for AI transformation. The PE consortium provides a built-in pipeline through portfolio companies. Whether the unit economics work in practice is unproven, but the option now exists where it did not last week.

Continue Reading

AI Broke SaaS. Services Is the Escape Hatch.

AI breaks the SaaS replication engine. Sequoia's Julien Bek argues the next $1T company sells the work itself, not the tool. The autopilot model is the architectural escape hatch.

Build Once, Sell Many. AI Just Broke That.

The software model works because you build once and sell many times. Enterprise data restrictions are breaking that replication engine for AI companies.

The Unbundling of LLMs

LLM wrappers get dismissed. But the companies building real workflow around foundation models are following the same pattern that created billion-dollar SaaS companies.

Evaluating an AI-native services pitch?

I help mid-market operators figure out which AI services vendors are worth a meeting and which are repackaged consulting. Let's talk.

Let's Talk