AI Broke SaaS. Services Is the Escape Hatch.

President, Zaruko

Table of Contents

The SaaS model that built every software fortune of the last twenty years runs on replication economics. Build once, sell many, marginal cost approaches zero, gross margins land at 80 to 90 percent. That engine is what made software the best business model ever invented.

AI breaks the engine.

On April 3, 2026, I wrote that the data which used to flow from clients to vendors and compound into a moat increasingly sits behind contractual restrictions in enterprise procurement templates.1 I laid out five outcomes for how the market might respond. The first, and the one I framed as the most damaging, was that every AI software deployment becomes a custom engagement. The economics collapse from software toward managed services. More custom, more fragmented, lower margins, harder to scale.

I framed Outcome 1 as a consequence. Something that happens to AI startups against their will.

A month earlier, Sequoia partner Julien Bek had published the offensive playbook for the same outcome. Different sign on the value judgment. He calls it Services: The New Software.2 The next $1T company, he argues, will be a software company masquerading as a services firm. Not selling the tool. Selling the work itself.

His essay went viral. It deserves the attention. And read alongside the data restriction problem, it points to something neither piece states explicitly.

The services model is the architectural escape hatch from the SaaS replication trap.

Bek's Framework, in One Pass

Bek splits work into two categories. Intelligence is anything with clear correct and incorrect answers. Coding, accounting rules, medical coding, NDA drafting, insurance brokerage form-filling, tax preparation. The rules are complex but they are rules. AI is rapidly crossing the threshold where it can do this work autonomously.

Judgment is taste, instinct, experience. Knowing what to build next. Reading a room. Assessing culture fit. Strategic recommendation. AI is not there yet, and may not be for a long time.

He then plots services categories on a second axis: already outsourced or done in-house. The wedge for an AI-native services firm is the intersection. Outsourced and intelligence-heavy. Replacing an outsourcing contract is a vendor swap. Replacing internal headcount is a reorg. The vendor swap path is dramatically lower friction.

Bek calls these AI-native services firms autopilots. A copilot sells a tool to a professional and lets the professional use it. Harvey sells to law firms. Rogo sells to investment banks. The professional remains responsible for the output. An autopilot sells the work directly. Crosby sells to the company that needs the NDA, not to outside counsel. WithCoverage sells to the CFO who needs insurance, not to the broker.

Bek's punchline is the math. For every dollar enterprises spend on software, they spend six on services.2 The total addressable market for autopilots is six times larger than the market for the SaaS tools that serve those same workers.

The List

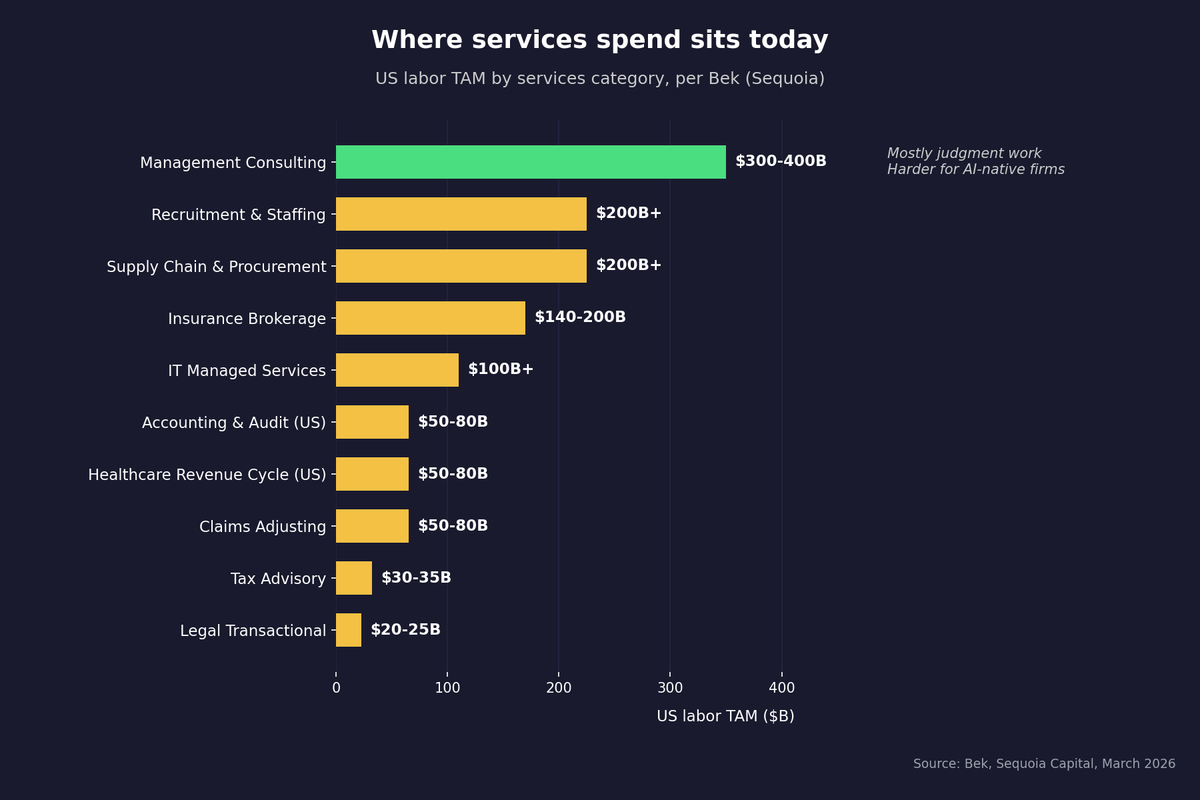

Bek maps the largest autopilot opportunities by category and US labor TAM:2

- Recruitment and staffing: $200B+

- Supply chain and procurement: $200B+

- Insurance brokerage: $140-200B

- IT managed services: $100B+

- Accounting and audit: $50-80B

- Healthcare revenue cycle: $50-80B

- Claims adjusting: $50-80B

- Tax advisory: $30-35B

- Legal transactional: $20-25B

- Management consulting: $300-400B (mostly judgment, harder)

Figure 1: US labor TAM by services category, sorted by size. Management consulting (green) is the largest market but most judgment-heavy, where the AI-native services model is harder to apply. Source: Bek, Sequoia Capital, March 2026.

Every line item on this list is a check a mid-market CFO writes today. To external vendors. For work that is mostly intelligence. The autopilot pitch is to replace those checks.

Why This Solves the Data Trap

The data restriction problem I wrote about on April 3 is simple to state. Enterprise clients increasingly contractually restrict AI vendors from using their operational data to train, fine-tune, or improve models.3 The clause shows up in master service agreements and procurement templates as a default. The information that used to flow from clients to vendors, get embedded into product roadmaps, and improve the software for the next client is no longer flowing.

That breaks the software replication engine. The contractual prohibition on training new models with Client A's data means the compounding moat that flowed from training on each new customer no longer accrues to the vendor. Each deployment becomes more isolated. The economics resemble managed services more than software. Bessemer reported that steadier-growth AI companies run around 60% gross margins, with the fastest-scaling cohorts averaging closer to 25%.4 Traditional SaaS runs 80-90%.

The autopilot model does not eliminate the data restriction problem. It changes where the boundary sits.

When the vendor is a SaaS provider, the customer's operational data is the customer's property. Training on it requires permission. The procurement clause exists because the data is going somewhere it should not.

When the vendor is the operator, the boundary changes. The autopilot delivering insurance brokerage runs the workflow and accumulates a running record of how cases get triaged, how exceptions get handled, and which patterns predict good outcomes. The vendor has a clearer claim to learn from its own operating process even where customer-specific data still requires negotiated rights. PHI, financial records, regulated transaction data, and similar sensitive inputs may still be restricted depending on the industry. But the operator-as-vendor structure leaves procurement with far less to restrict.

The replication engine does not return as pure SaaS. It returns as operational scale inside a services business. The autopilot's product improves through its repeatable patterns, exception handling, and workflow design, the same way an insurance broker improves on her own book of business. Six times the TAM, lower margins, but better margins than people assume. Bek cites Bret Taylor's Sierra running at 70% gross margins on AI-delivered customer service.5 WithCoverage selling 10x per human expert what a traditional broker sells.

The open question is whether these firms achieve true operational scale or simply become more efficient versions of traditional outsourcing businesses. Some will. Many will not. The thesis only works for the ones that do.

This is not a coincidence. It is the architectural answer to the structural problem.

What the Autopilot Model Cannot Fix

Three things.

Go-to-market does not scale like software. You cannot run a product-led growth motion for an autopilot that handles a customer's audit. You sell it the way services firms have always sold themselves. Relationships, references, partner channels, RFPs. Bek concedes this in his essay.2 It is the unsolved cost of the model.

Inference economics are not software economics. Foundation model providers control the underlying token cost, and pricing changes through token rates, usage caps, and packaging directly affect autopilot margins. Recent moves illustrate how externally controlled inference pricing can compress those margins: Anthropic capping token consumption during peak hours and OpenAI shifting Codex from per-message to per-token billing.5 Sierra's 70% margin assumes inference at current prices. The economics can move in either direction.

Accountability does not disappear. When the vendor sells the work, it inherits more responsibility for errors, compliance failures, and operational outcomes than a SaaS provider ever carried. A misfiled tax return, a botched insurance claim, a missed prior authorization is now the autopilot's problem, not the customer's. Insurance, audit trails, and regulatory exposure all increase. The economics have to absorb that cost.

All three are real. None of them invalidates the model. They cap the upside.

What This Means for Mid-Market Operators

The intelligence-heavy line items your company outsources today are targets. Not in some distant future. Now. There are funded autopilot startups in every category Bek lists.

The buy-vs-build conversation that has dominated mid-market AI strategy for two years was always asking the wrong question. The actual question is closer to: which of the checks we already write to outside vendors is going to have an AI-native competitor first, and what happens to our cost structure and our incumbent relationships when it does.

The list of likely first movers is not mysterious. It is the categories where the work is most intelligence-heavy and the customer relationship is most fragmented. IT managed services. Tax advisory. Insurance brokerage. Standard-line claims handling. Routine legal transactional work. The companies serving these markets are about to face price competition from operators that did not exist 18 months ago.

The decision to evaluate them is not a long-term planning exercise. It is a 2026 procurement question.

Where This Goes Next

Bek's essay is the framework. The autopilot model is the architectural escape hatch from the SaaS replication trap.

The thesis is no longer just academic. Two of the largest LLM providers have already bet at scale on what comes next. OpenAI announced Frontier Alliances with BCG, McKinsey, Accenture, and Capgemini in February. Anthropic announced a new enterprise AI services joint venture with Blackstone, Goldman Sachs, and Hellman & Friedman this past Monday, reportedly backed by approximately $1.5 billion in committed capital. Different mechanics, same destination.

That is the next post.

Sources

- Damianakis, Stefanos. "Build Once, Sell Many. AI Just Broke That." Zaruko, April 3, 2026. zaruko.com. ↑

- Bek, Julien. "Services: The New Software." Sequoia Capital, March 2026. sequoiacap.com. ↑ ↑ ↑ ↑

- Debevoise and Plimpton. "AI's Biggest Enterprise Challenge in 2026: Contractual Use Limitations on Data." November 2025. debevoisedatablog.com. ↑

- Bessemer Venture Partners. "State of AI 2025." August 2025. ↑

- Kahn, Jeremy. "Are services the new software? This Sequoia partner thinks so." Fortune, April 21, 2026. fortune.com. ↑ ↑

Frequently Asked Questions

What is an AI autopilot, and how is it different from an AI copilot?

A copilot sells a tool to a professional and lets the professional use it. Harvey sells to law firms. Rogo sells to investment banks. The professional remains responsible for the output. An autopilot sells the work directly. Crosby sells to the company that needs the NDA, not to outside counsel. WithCoverage sells to the CFO who needs insurance, not to the broker. Sequoia partner Julien Bek argues the autopilot model is where the largest AI services opportunities sit, because for every dollar enterprises spend on software, they spend six on services.

Why does the services model escape the SaaS data restriction trap?

Enterprise procurement contracts increasingly prohibit AI vendors from using customer data to train or improve models, which breaks the SaaS replication engine. When the vendor is an operator rather than a software provider, the boundary changes. The autopilot accumulates a running record of how it triages cases, handles exceptions, and predicts outcomes inside its own operating process. The vendor has a clearer claim to learn from how it does the work, even where customer-specific inputs like PHI or financial records remain restricted. The replication engine returns as operational scale inside a services business.

Which services categories are most exposed to AI-native autopilots?

The categories most exposed are intelligence-heavy work that mid-market companies already outsource. Sequoia's Bek maps the largest US labor TAMs as recruitment and staffing ($200B+), supply chain and procurement ($200B+), insurance brokerage ($140-200B), IT managed services ($100B+), accounting and audit ($50-80B), healthcare revenue cycle ($50-80B), claims adjusting ($50-80B), tax advisory ($30-35B), and legal transactional work ($20-25B). Management consulting is the largest market at $300-400B but is mostly judgment work, which is harder for AI-native firms to attack.

Continue Reading

Build Once, Sell Many. AI Just Broke That.

The software model works because you build once and sell many times. Enterprise data restrictions are breaking that replication engine for AI companies.

The Unbundling of LLMs

LLM wrappers get dismissed. But the companies building real workflow around foundation models are following the same pattern that created billion-dollar SaaS companies.

74% Want Revenue from AI. 20% Are Getting It.

88% of companies have adopted AI. Fewer than 40% can point to a financial result. The gap between AI winners and everyone else is widening fast.

Evaluating an AI-native services vendor?

I help mid-market operators figure out which of the checks they write to outside vendors are about to face AI-native competition. Let's talk.

Let's Talk